|

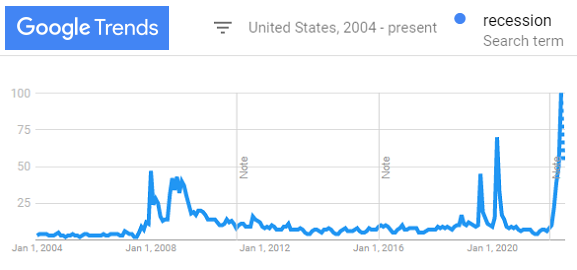

Last month, a YouGov poll in the USA found that 58% of Americans feel the economy is already in a recession.

Only 19% disagreed.

The bond market is also pointing towards a recession if not quite guaranteeing it just yet.

That's because, for now, the outlook for much steeper interest rates (such as this week's looming hike from the US Fed) won't quite take very short-term bond yields above longer-term rates. Not quite. Not yet.

But if that happens? Meaning when?

An inversion of 3-month Treasury bill rates above 10-year Treasury bond yields has presaged every US recession of the last 5 decades. It hasn't given a false signal since 1966. And maybe it is exactly what central banks want.

"A mild recession is probably pretty good from the Fed's point of view, given the situation we're in and how bad it looks," says former US Fed governor Laurance Meyer.

"In order to bring inflation down," agrees Austrian central-bank chief and ECB voting member Robert Holzmann, "you might have to accept a slight recession."

Got that?

Look, central banks can't do anything to end Russia's war on Ukraine. Nor can they do anything to ease the post-Covid supply-chain glitches causing product delays and surging costs either.

So to cap the overall pace of inflation, their best hope is to push down prices outside of those areas...

...destroying domestic demand in, say, the services sector by hiking the cost of borrowing.

"We hope that won't be necessary," says Holzmann.

But "we will go as far as necessary to ensure that inflation stabilises at our 2% target," said his ECB boss Christine Lagarde last month.

Whatever it takes? Hard to believe she's serious.

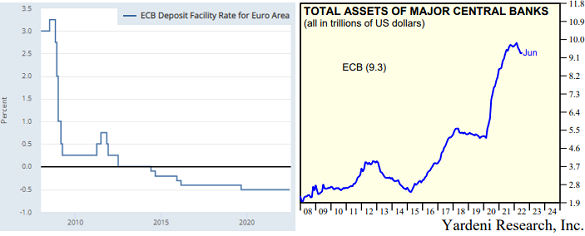

Last week the ECB raised Euro deposit rates from minus 0.5% up to...oh wow!...zero in the face of 8.6% annual inflation.

But this "front-loading" of policy rate rises "will support the return of inflation to our medium-term target by strengthening the anchoring of inflation expectations and by ensuring that demand conditions adjust to deliver our inflation target in the medium term," Lagarde claimed last Thursday.

Ensuring. Demand. Conditions. Adjust.

Not quite "whatever it takes". But then suggesting you want to provoke a recession is more controversial today even than trying to rescue over-stretched debtors a decade ago. And more sad still for Lagarde and her ECB team, that's also something which they now want to achieve as well. They're just as coy about this as they are about recession.

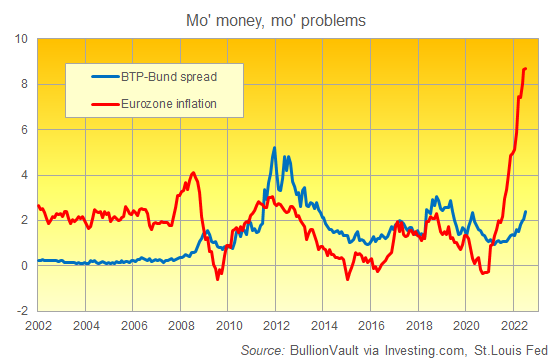

"On Italy, we are seeing yields rising with the political uncertainty at centre stage," said a journalist at last Thursday's ECB press conference.

"What's your message to the market?"

"Very confused," came the answer, if not in so many words.

The ECB has given itself a new facility which means that...even while it halts new QE money creation and bond buying as it raises interest rates...it can also create new money and buy bonds at will.

"Under this Transmission Protection Instrument, all members of the Euro area can be eligible," said Lagarde. "All of them."

So that means Italy?

"The Governing Council, in its discretion, in its assessment, will determine on the basis of the eligibility criteria, on the basis of the indicators that will signal or not unwarranted, disorderly market dynamics, whether or not a country is eligible and whether it activates the TPI. Voilà."

Got it? Voilà.

Other journalists tried to press the point, asking a further 3 times whether Italy was about to get emergency TPI QE to rescue its government bond market ahead of September's snap election, when the anti-Euro Brothers of Italy look set to come first but lack a majority.

Not once was the country named by Lagarde or Luis de Guindos, her vice-president. And they were only a little less coy about the economic impact of their interest-rate rises.

"Under [our] baseline scenario there is no recession, neither this year nor next year. [But] is the horizon clouded? Of course it is."

Whatever it takes? Yeah, well, like, whatever.

Central banks were the wind beneath the wings of the financial markets and global economy during the financial crisis. They blew hard at keeping things afloat during Covid as well, aided by record-heavy government borrowing and stimulus.

So a decade on from Draghi's dramatic vow, the scope and size of monetary policy now runs far and away beyond anything investors could have imagined in July 2012.

What it will take to rein in those powers, and leave the economy to fly or crash by itself, is anyone's guess.

|